Car Insurance for Young Drivers: Everything You Need to Know

Different Types of Home Insurance Policies (2025 Guide)

April 29, 2025

Auto Insurance Requirements in California (2025 Update)

May 7, 2025

Car insurance is typically more expensive for young drivers due to their limited driving history and statistically higher risk of accidents. Insurance providers assess premiums based on age, experience, and driving behavior—areas where teen and first-time drivers often fall short.

In this guide, you’ll learn what coverage young drivers need, what affects their insurance rates, legal requirements by state, and actionable ways to save. All insights are based on data from the Insurance Information Institute (III) and NAIC.

I created this guide to help young drivers—and their parents—make informed decisions through accurate comparisons and expert-backed strategies.

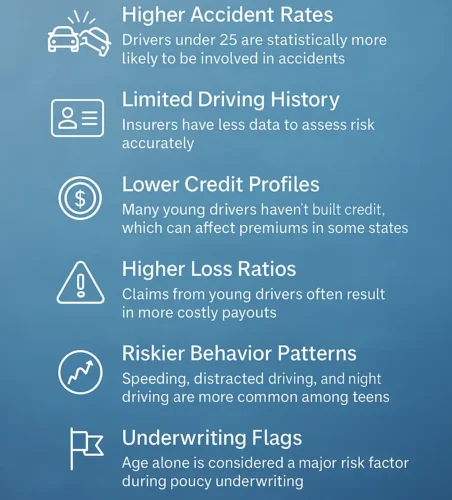

Why Car Insurance Is More Expensive for Young Drivers

Young drivers face higher insurance costs because insurers consider them a higher risk based on real-world data and underwriting models.

- Higher accident rates: Drivers under 25 are statistically more likely to be involved in accidents.

- Limited driving history: Insurers have less data to assess risk accurately.

- Lower credit profiles: Many young drivers haven’t built credit, which can affect premiums in some states.

- Higher loss ratios: Claims from young drivers often result in more costly payouts.

- Riskier behavior patterns: Speeding, distracted driving, and night driving are more common among teens.

- Underwriting flags: Age alone is considered a major risk factor during policy underwriting.

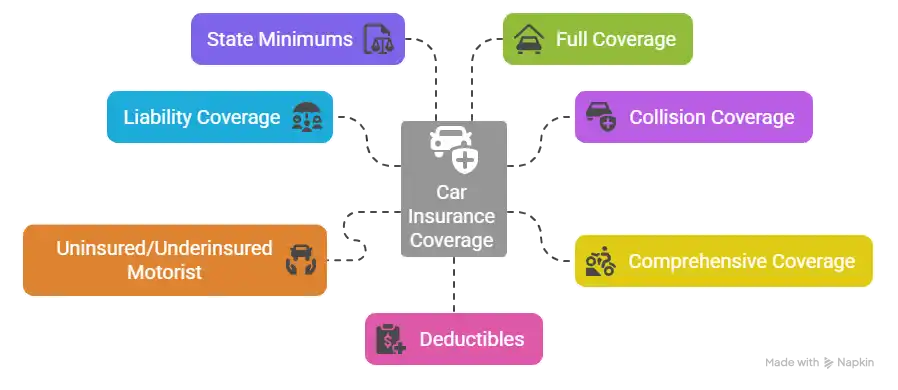

What Type of Car Insurance Do Young Drivers Need?

Choosing the right type of car insurance is essential for meeting legal requirements and protecting against unexpected costs.

- Liability coverage: Required in most states to cover bodily injury and property damage to others.

- Collision coverage: Pays for damage to your car from accidents, regardless of fault.

- Comprehensive coverage: Covers non-collision events like theft, vandalism, or weather damage.

- Uninsured/underinsured motorist: Protects you if the at-fault driver doesn’t have enough coverage.

- State minimums vary: Each state has different liability limits that must be met by law.

- Full coverage is ideal: Recommended for new cars or when financial protection is a priority.

- Deductibles matter: A higher deductible lowers premiums but increases out-of-pocket costs.

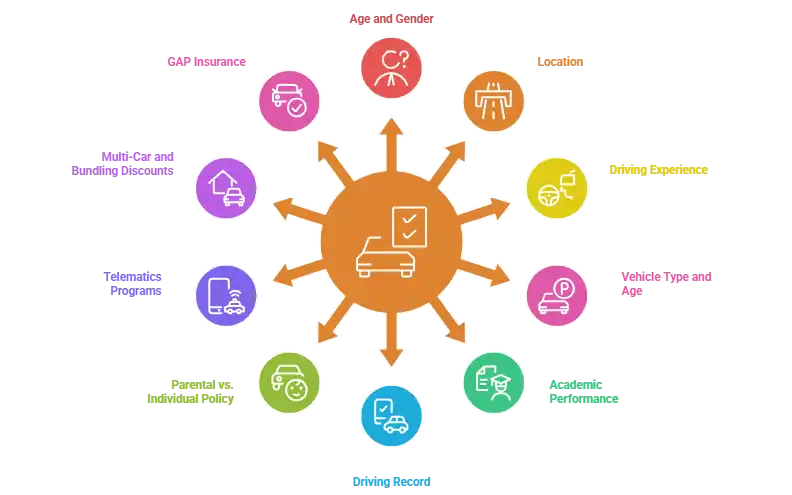

Factors That Affect Car Insurance Rates for Young Drivers

Several personal and vehicle-related factors influence how much a young driver pays for insurance.

- Age and gender: Younger males often face higher premiums due to higher risk profiles.

- Location: Urban areas usually have higher rates due to traffic and theft risk.

- Driving experience: Less time on the road means higher perceived risk.

- Type and age of vehicle: Sports cars and newer models usually cost more to insure.

- Academic performance: Good grades can qualify students for discounts.

- Driving record: Tickets, claims, or accidents quickly raise insurance costs.

- Parental vs. individual policy: Staying on a parent’s plan can often be more affordable.

- Telematics programs: Safe driving tracked by apps or devices can lower rates.

- Multi-car and bundling discounts: Insuring multiple vehicles or combining with home insurance can reduce costs.

- GAP insurance: May be needed if the car is financed and depreciates faster than the loan balance.

How to Lower Car Insurance Costs as a Young Driver?

With the right strategies, young drivers can reduce their insurance premiums without sacrificing coverage.

- Good student discounts: Many insurers offer lower rates for maintaining a high GPA.

- Defensive driving courses: Completing an approved course can lead to discounts.

- Telematics and usage-based insurance: Programs track driving habits and reward safe behavior.

- Pay-per-mile insurance: Ideal for drivers who don’t use their car often.

- Compare quotes regularly: Use insurance aggregators to find the best deal.

- Choose a practical car: Safe, older, and modestly priced vehicles cost less to insure.

- Join a parent’s policy: Often cheaper than getting a standalone policy.

- Avoid traffic violations: A clean record helps maintain lower rates over time.

Best Car Insurance Companies for Young Drivers (with Pros & Cons)

Choosing the right insurer can significantly impact both coverage quality and cost. Below is a comparison of top providers based on average premiums, discounts, and program features tailored for young drivers.

|

Insurance Company |

Average Annual Premium (18–19 years old) |

Key Discounts & Features |

Pros |

Cons |

|

GEICO |

$1,342–$3,891 |

Good student, multi-vehicle, military, and alumni discounts. Telematics program available. |

Competitive rates, especially for teens. Strong mobile app and online tools. |

Limited availability of the telematics program in all states. |

|

State Farm |

$1,404–$4,565 |

Good student, driver training, and student-away-from-home discounts. |

Excellent customer service and claims satisfaction. Offers a telematics program for safe driving. |

Higher average premiums compared to some competitors. |

|

Progressive |

$1,413–$6,022 |

Snapshot program for safe driving discounts. |

Innovative usage-based insurance with potential savings. Offers Name Your Price tool. |

Higher rates for young drivers compared to some competitors. |

|

USAA |

$2,656–$2,066 |

Exclusive to military families. Offers various discounts and benefits. |

Exceptional customer service and competitive rates for eligible members. |

Only available to military families. |

|

Travelers |

$2,966–$2,289 |

IntelliDrive program for safe driving discounts. |

Offers competitive rates and discounts for young drivers. |

Limited availability of the telematics program in all states. |

Mistakes Young Drivers Should Avoid When Getting Car Insurance

- Ignoring coverage needs: Skimping on essential coverage like liability or uninsured motorist, can lead to significant out-of-pocket costs.

- Not comparing enough quotes: Failing to shop around can result in paying more than necessary.

- Choosing a sports or luxury car: High-performance vehicles can lead to much higher premiums due to their cost and risk factors.

- Missing out on discounts: Discounts for good grades, safe driving, and bundling policies are often overlooked but can lower premiums.

- Not disclosing driving history accurately: Failing to provide complete information can lead to a premium hike or policy cancellation later.

- Letting coverage lapse: A gap in coverage can increase future premiums and may even result in difficulty getting insured.

- Excluding key drivers: Failing to list all potential drivers on the policy can create problems during a claim.

Expert Tips from Insurance Advisors

Here are some simple, high-authority tips from insurance professionals that can help young drivers save money and get the right coverage:

- Bundle policies when possible: Combining car insurance with other policies like renters' or homeowners can lower your overall premium.

- Choose a higher deductible carefully: A higher deductible can reduce monthly costs, but make sure you can afford it in case of a claim.

- Consider usage-based insurance: Telematics programs track driving habits and can reward safe drivers with lower premiums.

- Maintain a clean driving record: Avoiding tickets and accidents helps keep insurance rates low over time.

- Ask about all available discounts: Many insurers offer discounts for good grades, defensive driving courses, and low mileage.

Frequently Asked Questions

What is the cheapest auto insurance for young drivers?

GEICO and State Farm often offer the most affordable policies for young drivers, especially when discounts are applied.

Can a 17-year-old get their car insurance?

Yes, but it’s usually more expensive; being added to a parent’s policy is often more cost-effective.

What’s the cheapest car to insure for a young driver?

Older, reliable sedans like the Honda Civic or Toyota Corolla tend to have lower premiums.

Is it cheaper to be on your parents’ car insurance?

Yes, premiums are typically lower when young drivers are added to a parent’s existing policy.

Does car insurance go down at 25?

Generally, yes—if you maintain a clean driving record, premiums often decrease significantly around age 25.

Why is car insurance so expensive for young drivers?

Due to limited driving history and statistically higher accident rates, insurers consider young drivers high-risk.

Conclusion

Getting car insurance as a young driver can feel overwhelming, but understanding your coverage options, comparing quotes, and avoiding common mistakes can make a big difference.

Safe driving habits not only keep you protected but also help lower your premiums over time.

Take the next step: use a comparison tool or talk to a licensed insurance agent to find a policy that fits your needs and budget.

{kind=link}

{kind=link}

{kind=link}