What Is Homeowners Insurance and Why Is It Important?

How Does Car Insurance Work in Simple Terms?

April 17, 2025

Different Types of Home Insurance Policies (2025 Guide)

April 29, 2025

Imagine waking up one morning, only to find your car missing with no insurance coverage to rely on. It is a stressful and overwhelming situation that can happen to anyone.

In this guide, I will explain what realistically happens when your car is stolen without insurance, what immediate actions you should take, and how you can better protect yourself in the future.

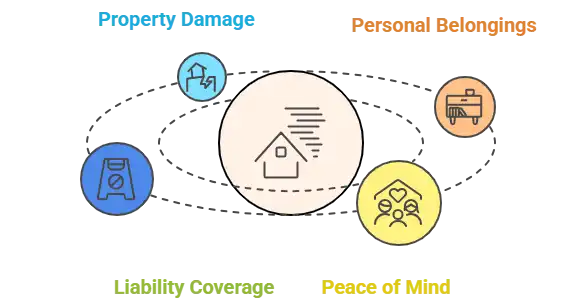

What Is Homeowners Insurance?

Homeowners' insurance is a type of policy that protects you financially if your home or belongings are damaged, stolen, or destroyed. If someone gets injured on your property and sues you, it also covers you.

A typical homeowners' insurance policy covers the structure of your home, your personal belongings, liability protection, and additional living expenses if you need to live elsewhere while your home is being repaired.

Standard coverages are included in most policies, but you can also add optional protections like flood insurance, earthquake coverage, or extended personal property coverage, depending on your needs.

Why Is Homeowners Insurance Important?

Homeowners insurance is more than just coverage for your house. It protects your finances, provides legal security, and offers peace of mind when unexpected events happen.

- Financial protection against large, unexpected losses: Homeowners insurance helps cover major expenses from events like fires, storms, or theft, preventing devastating out-of-pocket costs.

- Required by mortgage lenders in most cases: Most lenders require homeowners insurance to protect their investment while you are paying off your mortgage.

- Legal and personal peace of mind: It shields you from legal claims if someone gets injured on your property and provides peace of mind knowing you are protected.

- Protection beyond just rebuilding the home: Policies often cover additional costs like legal fees, temporary housing, and replacement of stolen belongings, offering broader security.

What Are the Key Components of a Homeowners Insurance Policy?

A homeowners' insurance policy is made up of several important parts that work together to fully protect you and your property.

- Dwelling Coverage: Protects the structure of your home, including walls, roof, and built-in appliances, against covered damages.

- Personal Property Coverage: Covers personal belongings like furniture, clothing, and electronics if they are stolen or damaged.

- Liability Protection: Helps cover legal expenses and damages if someone is injured on your property or if you accidentally cause damage to others' property.

- Additional Living Expenses (ALE): Pays for temporary living costs, such as hotel stays and meals, if your home becomes uninhabitable due to a covered event.

- Other Structures Coverage: Protects detached structures on your property, like garages, fences, and sheds.

What Events Does Homeowners Insurance Cover?

Homeowners insurance protects you against a variety of common risks that can cause major financial losses.

- Fires and Smoke Damage: Covers damages to your home and belongings caused by fire or smoke.

- Storms (Wind, Hail, Lightning): Protects against physical damage from severe weather events like strong winds, hailstorms, and lightning strikes.

- Theft and Vandalism: Covers loss or damage if your property is stolen or intentionally damaged.

- Certain Types of Water Damage: Protects against sudden water damage like burst pipes, but usually does not cover flooding from natural disasters.

- Liability Claims: Covers medical bills and legal costs if someone is injured on your property or if you accidentally damage someone else's property.

What Homeowners Insurance Typically Doesn’t Cover

While homeowners insurance covers many risks, there are important exclusions you should know about to avoid surprises.

- Floods: Standard policies do not cover flood damage. You need a separate flood insurance policy.

- Earthquakes: Earthquake damage requires separate coverage, usually through a specialized policy or rider.

- Wear and Tear or Maintenance Issues: Insurance does not cover problems caused by neglect or normal aging of your home.

- Certain Types of Infestations: Damage from pests like termites or rodents is generally excluded from coverage.

How Much Homeowners Insurance Do You Need?

Choosing the right amount of homeowners insurance is critical to fully protect your home and belongings without overpaying for coverage.

|

Factor |

Explanation |

|

Home Value |

Your coverage should be enough to rebuild your home completely at current construction costs. |

|

Belongings |

Consider the total value of personal property like furniture, electronics, and clothing. |

|

Location Risks |

High-risk areas for floods, earthquakes, or crime may require additional coverage or endorsements. |

|

Replacement Cost vs. Actual Cash Value |

Replacement cost policies cover full rebuilding costs, while actual cash value accounts for depreciation. Replacement cost is often better for full protection. |

|

Policy Reviews |

Reviewing your policy annually ensures your coverage keeps up with changes in home value, renovations, or new purchases. |

Common Myths About Homeowners Insurance

Many people misunderstand what homeowners insurance covers. Here are some common myths and the reality behind them:

- "It covers everything."

Reality: Standard policies have exclusions like floods, earthquakes, and maintenance issues. - "Only homeowners with mortgages need it."

Reality: Even if you own your home outright, insurance protects you from major financial losses. - "Insurance automatically covers full rebuild costs."

Reality: Without a replacement cost policy, you might only get the depreciated value, not enough to rebuild.

Tips for Choosing the Right Homeowners Insurance Policy

Selecting the right homeowners insurance requires more than just picking the cheapest option. Here are important tips to guide you:

- Compare multiple providers and policies.

Look at coverage options, exclusions, and customer reviews to find the best fit. - Understand deductibles and policy limits.

Know how much you will pay out of pocket and what your maximum coverage amounts are. - Ask about bundling discounts (auto + home).

Combining policies can often lower your overall insurance costs. - Check financial strength ratings of insurers.

Choose companies with strong financial ratings to ensure they can pay claims when needed. - Review coverage yearly as needs change.

Update your policy after major life events, renovations, or increases in home value.

FAQs About Homeowners Insurance

What does homeowners insurance actually protect?

It covers your home's structure, personal belongings, liability for injuries, and additional living expenses if your home becomes uninhabitable.

Do you need homeowners insurance if your house is paid off?

Yes, it is still highly recommended to protect your investment from unexpected damages, theft, or liability claims.

How are home insurance rates calculated?

Rates depend on factors like your home's value, location, construction type, coverage limits, and your claims history.

Can you change home insurance providers anytime?

Yes, you can switch providers at any time, even mid-policy. Just ensure there is no lapse in coverage.

What’s the difference between homeowners insurance and mortgage insurance?

Homeowners insurance protects your home and belongings, while mortgage insurance protects the lender if you default on your loan.

Conclusion

In summary, without auto insurance, you are fully liable for the financial loss if your car is stolen. You would also remain responsible for any remaining loan balance on the vehicle, even if it is not recovered. It’s crucial to safeguard yourself from these risks by selecting the appropriate coverage.

To protect your future and ensure peace of mind, consider obtaining a personalized quote by completing a short form.

{kind=link}

{kind=link}

{kind=link}